黄金科学技术 ›› 2020, Vol. 28 ›› Issue (3): 380-390.doi: 10.11872/j.issn.1005-2518.2020.03.001

郑明贵1,2( ),曾健林1()

),曾健林1()

Minggui ZHENG1,2(),Jianlin ZENG1()

摘要:

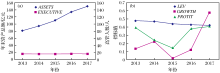

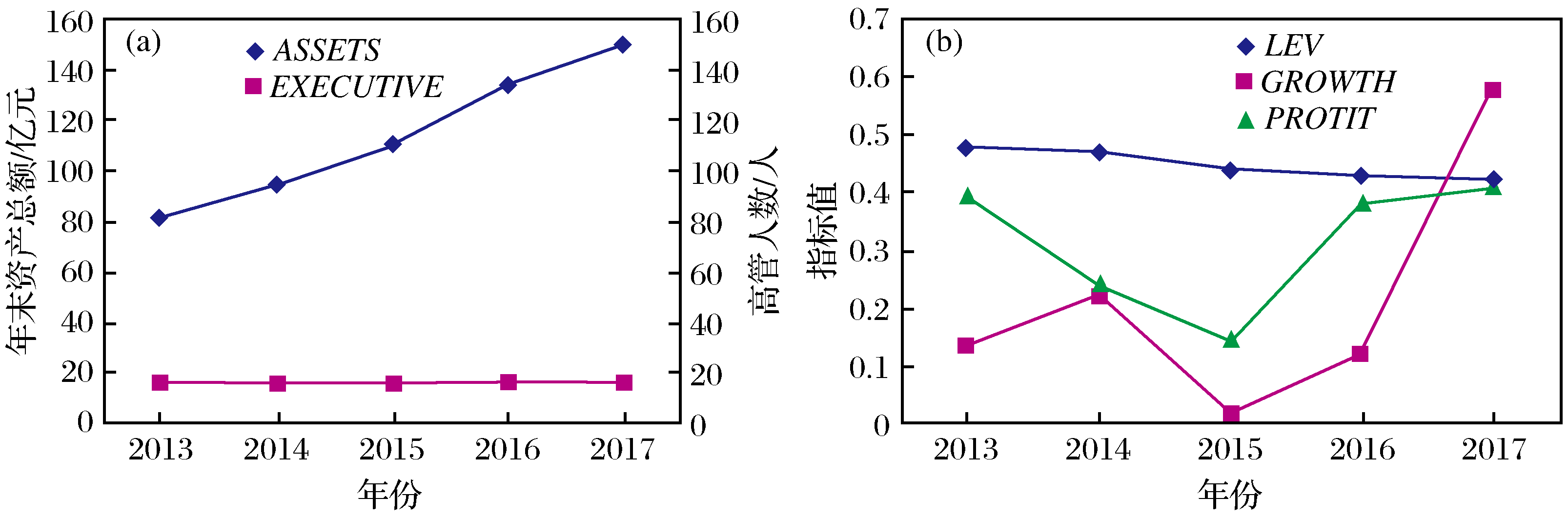

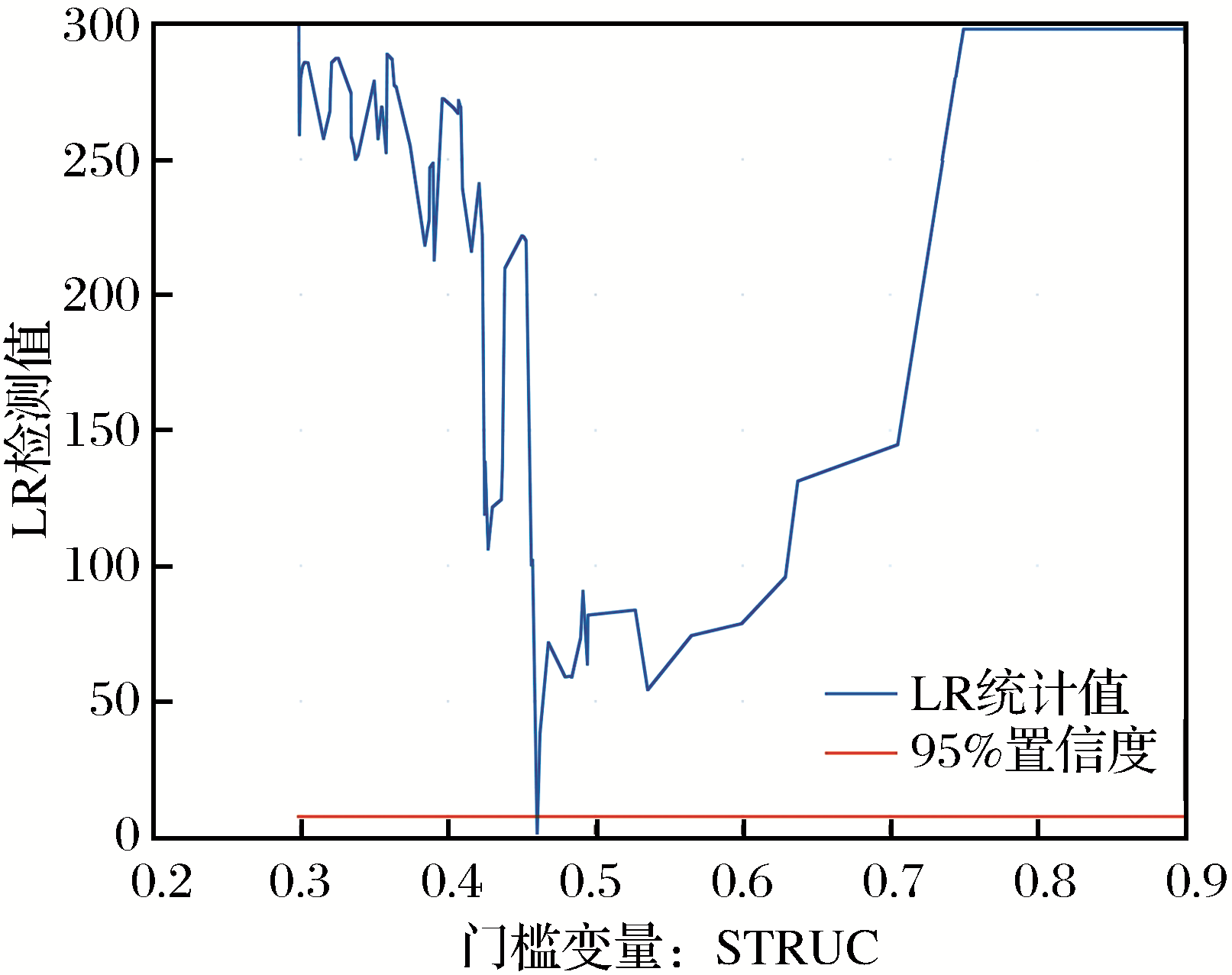

利用中国沪深上市私营矿业公司2013~2017年数据,考察了股权集中度与中国私营矿业公司治理效率之间的关系。考虑到股权集中度与中国私营矿业公司治理效率之间可能存在门槛效应,建立了中国私营矿业公司治理效率DEA评价模型、股权集中度与中国私营矿业公司治理效率门槛模型。研究发现:(1)股权集中度与中国私营矿业公司治理效率之间存在门槛效应和倒“U”型关系。当股权集中度低于门槛值29.73%时,股权集中度与公司治理效率呈现正相关;当股权集中度高于门槛值29.73%时,股权集中度与公司治理效率呈现负相关。(2)中国私营矿业公司最大股东最优控股比例位于[0.1873,0.3360]区间。(3)公司规模与中国私营矿业公司治理效率呈现负相关。

中图分类号:

| 1 | 杨晓光,杨翠红.2015年中国经济形势展望及预测[J].中国科学院院刊,2015,30(1):1-7. |

| Yang Xiaoguang, Yang Cuihong.Prospect of China’s economy in 2015 and its macroeconomic forecasting [J]. Bulletin of Chinese Academy of Sciences, 2015, 30(1): 1-7. | |

| 2 | 李维安,李汉军.股权结构、高管持股与公司绩效——来自民营上市公司的证据[J].南开管理评论,2006,9(5):4-10. |

| Li Wei’an, Li Hanjun.Ownership structure, executive ownership and performance:Evidence from private listed firms in China[J].Nankai Business Review,2006,9(5): 4-10. | |

| 3 | 杨波,唐小我,马永开.股权结构与公司治理效率研究[J].软科学,2004,18(1):61-63. |

| Yang Bo,Tang Xiaowo,Ma Yongkai.The relation bet-ween the equity ownership structure and corporation governance [J]. Soft Science, 2004, 18(1): 61-63. | |

| 4 | 蒋建湘.我国国有公司股权结构及其法律改革——以公司治理效率为主要视角[J].法律科学(西北政法大学学报),2012,30(6):131-138. |

| Jiang Jianxiang.State-owned corporation’s ownership structure and its legal reform: A view from corporation governance efficiency[J].Science of Law(Journal of Nor-thwest University of Political Science and Law),2012, 30(6): 131-138. | |

| 5 | 李维安.国际经验与企业实践——制定适合国情的中国公司治理原则[J].南开管理评论,2001,4(1):4-8. |

| Li Wei’an.Call for corporate governance principles of China fit for situation of our country [J]. Nankai Business Review, 2001,4(1): 4-8. | |

| 6 | 吉林大学中国国有经济研究中心课题组.治理效率:一个深化公司治理的新视角[J].当代经济研究,2002(12):8-14. |

| Center for China Public Sector Economy Research of Jilin University.Governance efficiency: A new perspective to deepen corporate governance[J].Contemporary Economic Research,2002(12):8-14. | |

| 7 | 郭婧.政府干预、终极股权结构与公司治理效率[D].太原:山西财经大学,2017. |

| Guo Jing. Government Intervention,Ultimate Ownership Structure and Efficiency of Corporate Governance [D]. Taiyuan:Shanxi University of Finance and Economics,2017. | |

| 8 | Tobin J. A general equilibrium approach to monetary theory [J]. Journal of Money,Credit and Banking,1969, 1(1):15-29. |

| 9 | Mcconnell J J, Servaes H. Additional evidence on equity ownership and corporate value[J].Journal of Financial Economics,1990,27(2):595-612. |

| 10 | 蔡吉甫,陈敏.控制权性质、管理层持股与公司治理效率[J].产业经济研究,2005(3):16-22. |

| Cai Jifu,Chen Min.The relationship between attribute of control rights and shareholdings of managers and the governance efficiency of Chinese listed companies [J]. Industrial Economics Research,2005(3):16-22. | |

| 11 | 郑家喜.资本结构对家族上市公司治理效率影响的实证研究[J].管理世界,2007(9):168-169. |

| Zheng Jiaxi. Empirical research on the impact of capital structure on the governance efficiency of family listed companies [J]. Management World,2007(9):168-169. | |

| 12 | 庄学敏.股权流动性与公司治理效率研究[J].经济问题探索,2008(11):173-178. |

| Zhuang Xuemin. Research on equity liquidity and corporate governance efficiency [J]. Inquiry into Economic Issues, 2008(11):173-178. | |

| 13 | 王季.控制权配置与公司治理效率——基于我国民营上市公司的实证分析[J].经济管理,2009,31(8):45-51. |

| Wang Ji. Control right allocation and the corporate governance efficiency—Emprirical analysis based on Chinese private listed companies [J]. Business Management Journal, 2009,31(8):45-51. | |

| 14 | 贺小刚,李新春,连燕玲,等.家族内部的权力偏离及其对治理效率的影响——对家族上市公司的研究[J].中国工业经济,2010(10):96-106. |

| He Xiaogang, Li Xinchun, Lian Yanling, et al. Power deviation among family agents and its effect on firm value—An empirical study in China [J]. China Industrial Economics,2010(10):96-106. | |

| 15 | Kang Y S, Kim B Y. Ownership structure and firm performance:Evidence from the Chinese corporate reform [J]. China Economic Review,2012,23(2):471-481. |

| 16 | 吕新军.股权结构、高管激励与上市公司治理效率——基于异质性随机边界模型的研究[J].管理评论,2015,27(6):128-139. |

| Xinjun Lü.Ownership structure,executive incentive and listed corporation governance efficiency[J].Management Review,2015,27(6):128-139. | |

| 17 | Charnes A,Cooper W W,Rhodes E. Measuring the efficiency of decision making units [J]. European Journal of Operational Research,1978,2(6):429-444. |

| 18 | Lauterbach B,Vaninsky A.Ownership structure and firm performance:Evidence from israel [J]. Journal of Management and Governance,1999,3(2):189-201. |

| 19 | Lehmann E,Warning S,Weigand J. Governance structures,multidimensional efficiency and firm profitability [J].Journal of Management and Governance,2004,8(3):279-304. |

| 20 | 刘文虎.基于数据包络分析法的公司治理及其效率评价研究[J].证券市场导报,2012(11):62-67. |

| Liu Wenhu.Research on corporate governance and efficiency evaluation based on data envelopment analysis [J]. Securities Market Herald,2012(11):62-67. | |

| 21 | 苏顺海,李小健.我国上市公司治理效率影响因素研究——基于DEA-Tobit两步法的实证分析[J].广西社会科学,2014(7):71-75. |

| Su Shunhai,Li Xiaojian.Research on the factors affecting the governance efficiency of China’s Listed companies: An empirical analysis based on the two-step method of DEA-Tobit [J]. Social Sciences in Guangxi,2014(7):71-75. | |

| 22 | 雷辉,龙辉.我国上市公司治理效率——基于DEA方法[J].系统工程,2016,34(11):17-23. |

| Lei Hui,Long Hui.The governance efficiency of listed companies in China—Based on DEA[J]. Systems Engineering, 2016,34(11):17-23. | |

| 23 | Berle A A,Means G C.The Modern Corporation and Private Property [M]. New York:Mc-Millan Press,1932. |

| 24 | Jensen M C,Meckling W H. Theory of the firm:Managerial behavior,agency costs and ownership structure [J]. Journal of Financial Economics,1976,3(4):305-360. |

| 25 | 姜冰雨,李伟.上市公司的股权结构与治理效率分析[J].理论探讨,2000(6):49-51. |

| Jiang Bingyu,Li Wei.Analysis of equity structure and governance efficiency of listed companies[J].Theoretical Investigation,2000(6):49-51. | |

| 26 | 马连福.股权结构的适度性与公司治理效率[J].南开管理评论,2000(4):19-23. |

| Ma Lianfu. Moderation of equity ownership structure and efficiency of corporate governance[J].Nankai Business Review, 2000(4):19-23 | |

| 27 | 朱武祥,宋勇.股权结构与企业价值——对家电行业上市公司实证分析[J].经济研究,2001(12):66-72. |

| Zhu Wuxiang, Song Yong. Equity structure and firm value:An empirical analysis of listed companies of household electric appliances industry [J]. Economic Research Journal,2001(12):66-72. | |

| 28 | 朱红军,汪辉.“股权制衡”可以改善公司治理吗?——宏智科技股份有限公司控制权之争的案例研究[J].管理世界,2004(10):114-123. |

| Zhu Hongjun,Wang Hui.Can “check-and-balance of stock ownership” improve company’s control?—A case study of struggle for the controlling right of Hongzhi Science and Technology Limited Company[J].Management World, 2004(10):114-123. | |

| 29 | 邱闯,李延喜,李艺玮.公司治理水平对多元化上市公司价值增长的影响研究[J].当代经济管理,2013,35(12):92-97. |

| Qiu Chuang,Li Yanxi,Li Yiwei. The study on the effect of corporate governance on the value growth of diversified listed companies[J].Contemporary Economic Management,2013,35(12):92-97. | |

| 30 | 杜莹,刘立国.股权结构与公司治理效率:中国上市公司的实证分析[J].管理世界,2002(11):124-133. |

| Du Ying,Liu Liguo.Ownership structure and corporate governance efficiency:An empirical analysis of Chinese listed companies [J]. Management World,2002(11):124-133. | |

| 31 | 吴淑琨.股权结构与公司绩效的U型关系研究——1997~2000年上市公司的实证研究[J].中国工业经济,2002(1):80-87. |

| Wu Shukun.Ownership structure and firm performance:An empirical research on Chinese public companies [J]. China Industrial Economics,2002(1):80-87. | |

| 32 | 蔡吉甫,杨智杰.内部人持股与公司治理效率关系研究[J].当代经济管理,2005,27(4):142-147. |

| Cai Jifu,Yang Zhijie.The relationship between shareholdings of insiders and the governance efficiency of listed companies:An empirical study[J].Contemporary Econo-mic Management,2005,27(4):142-147. | |

| 33 | 朱明秀.第一大股东性质、股权结构与公司治理效率研究[J].统计与决策,2005(23):112-114. |

| Zhu Mingxiu.Research on the nature of the first largest shareholder,ownership structure and corporate governance efficiency[J].Statistics & Decision,2005(23):112-114. | |

| 34 | 白重恩,刘俏,陆洲,等.中国上市公司治理结构的实证研究[J].经济研究,2005(2):81-91. |

| Bai Chong’en,Liu Qiao,Lu Zhou,et al. An empirical study on Chinese listed firms’ corporate governance [J]. Economic Research Journal,2005(2):81-91. | |

| 35 | 夏纪军.股权集中度与公司治理绩效[J].世界经济文汇,2017(3):46-63. |

| Xia Jijun. Ownership concentration and corporate governance performance[J].World Economic Papers,2017(3): 46-63. | |

| 36 | 夏鸿义,李永壮,张倩颖,等.内部审计质量、公司规模与公司绩效——基于上市公司面板数据的实证研究[J].中央财经大学学报,2016(6):71-78. |

| Xia Hongyi,Li Yongzhuang, Zhang Qianying,et al. Internal audit quality, enterprise scale and corporate performance:Empirical study of listed companies based on panel data[J].Journal of Central University of Finance and Economics,2016(6):71-78. | |

| 37 | Banker R D. Estimating most productive scale size using data envelopment analysis [J]. European Journal of Operational Research,1984,17(1):35-44. |

| 38 | 黄少安,张岗.中国上市公司股权融资偏好分析[J].经济研究,2001(11):12-20. |

| Huang Shao’an,Zhang Gang. Analysis of equity financing preference of Chinese listed companies [J]. Economic Research Journal,2001(11):12-20. | |

| 39 | 陆渊.基于数据包络分析法的中国保险公司治理研究[J].保险研究,2009(4):24-29. |

| Lu Yuan.Research on governance of Chinese insurance companies based on data envelopment analysis [J]. Insurance Studies,2009(4):24-29. | |

| 40 | 郑少锋,黄庆华.基于DEA方法的上市公司财务治理效率评价[J].经济问题,2011(10):58-61. |

| Zheng Shaofeng,Huang Qinghua. Evaluation on the efficiency of financial governance of listed companies under split share structure reform by data envelope analysis [J]. On Economic Problems,2011(10):58-61. | |

| 41 | 陈维政,胡豪,刘苹.基于企业产权关系的权变公司治理模式研究[J].南开管理评论,2008,11(1):91-98. |

| Chen Weizheng,Hu Hao,Liu Ping. Research on the contingency governance model based on relationship of firm property rights[J].Nankai Business Review,2008,11(1):91-98. | |

| 42 | 王怀明,史晓明.农业上市公司治理效率及对企业业绩的影响[J].农业技术经济,2010(5):64-70. |

| Wang Huaiming,Shi Xiaoming. Governance efficiency of agricultural listed companies and its impact on corporate performance[J].Journal of Agrotechnical Economics,2010(5):64-70. | |

| 43 | Hansen B E.Sample splitting and threshold estimation [J]. Econometrica,2000,68(3):575-603. |

| 44 | 孙永祥,黄祖辉.上市公司的股权结构与绩效[J].经济研究,1999(12):23-30. |

| Sun Yongxiang,Huang Zuhui.Equity structure and performance of listed companies[J].Economic Research Journal, 1999(12):23-30. | |

| 45 | 刘彬彬,陆迁,李晓平.社会资本与贫困地区农户收入——基于门槛回归模型的检验[J].农业技术经济,2014(11):40-51. |

| Liu Binbin,Lu Qian,Li Xiaoping.Social capital and farmers’ income in poor areas—A test based on threshold regression model[J].Journal of Agrotechnical Economics,2014(11):40-51. | |

| 46 | 余怒涛,沈中华,黄登仕.公司规模门槛效应下的董事会独立性与公司价值的关系[J].数理统计与管理,2010,29(5):871-882. |

| Yu Nutao,Shen Zhonghua,Huang Dengshi.The relation beween board independence and corporate value:Empirical analysis based on corporate size threshold effect [J]. Journal of Applied Statistics and Management,2010,29(5):871-882. | |

| 47 | 刘诚达.混合所有制企业大股东构成与企业绩效——基于企业规模门槛效应的实证检验[J].现代财经(天津财经大学学报),2019,39(6):15-26. |

| Liu Chengda.The composition of large shareholders and the performance of enterprises under mixed ownership—An empirical test based on the threshold effect of enterprise size[J].Modern Finance and Economics-Journal of Tianjin University of Finance and Economics,2019,39(6):15-26. | |

| 48 | 刘志彪.“股灾”反思和虚实经济协调发展的思考[J].东南学术,2015(6):4-11. |

| Liu Zhibiao.A reflection on “stock market crash” and some ideas on harmonious development of real and virtual economies[J].Southeast Academic Research,2015(6):4-11. | |

| 49 | 陈林,刘小玄.产业规制中的规模经济测度[J].统计研究,2015,32(1):20-25. |

| Chen Lin,Liu Xiaoxuan. Evaluating scale economy in the industry regulation[J].Statistical Research,2015,32(1):20-25. |

| [1] | 张顺堂, 李仲学. 基于DEA的黄金矿山经济效益评价模型研究[J]. J4, 2005, 13(05): 13-18. |

|

©2018 黄金科学技术编辑部

电话:0931-8277791

E-mail: hjkx@lzb.ac.cn 邮编:730000

甘公网安备 62010202000672号

甘公网安备 62010202000672号